A brief introduction to how cryptocurrency works is required to get a handle on the entire process. Bitcoin transactions include a sender and recipient, sum, timestamp, and cryptographic proof. The latter requires a significant amount of computing power to solve, and determines where a block belongs in the chain.

These blocks are held on multiple servers in different locations, so they are constantly updated. Once a transaction is made, it becomes publicly available on the blockchain. Find out how to use a privacy coin by checking out this content.

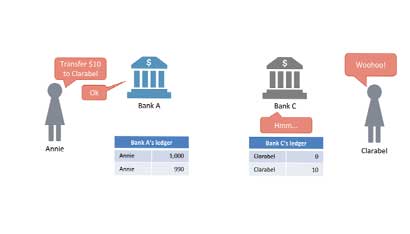

Decentralized Bank Ledger

The blockchain is like a decentralized bank ledger. All transactions are recorded in blocks, which are sent to all users that host a copy of the blockchain. Then, computers known as miners are rewarded for their work by adding new blocks to the ledger.

Each miner adds one block to the blockchain at a time, and the reward is distributed among all the miners. These miners sometimes pool their computers to increase the amount of transactions they can complete per second. The cryptocurrency community relies on consensus to keep the network running smoothly.

Blockchain Technology

As a result, a blockchain is similar to a decentralized bank ledger, a distributed database of all a transaction can be recorded. Every transaction is sent to all users hosting a copy of the blockchain. Those who successfully verify the blocks are called miners and receive rewards for their efforts. Since the technology behind cryptocurrencies is relatively new, there have been many versions of cryptocurrencies come and gone.

The first major version of Bitcoin came out in 2009, and the technology behind it continues to advance.

Online Transactions

The blockchain is a database of transactions. A blockchain is a digital currency. It is similar to a regular debit card. Despite its name, a cryptocurrency is nothing more than a virtual currency.

It is a database of transactions that is stored in a ledger. This is the same concept that powers a standard debit card. It is a digital version of cash. And the same principle applies to a cryptocurrency.

Provides Security

The ledger is the database of transactions, and every transaction is recorded. This ensures total visibility and prevents double-spending by preventing fraud. The ledger is a public record of all transactions and is open to the public.

It is also decentralized, meaning that no one owns the ledger. So, while it may seem complicated to use, it is a highly secure method of making online payments. A blockchain is also used to store digital assets.

Utilizes Smart Contracts

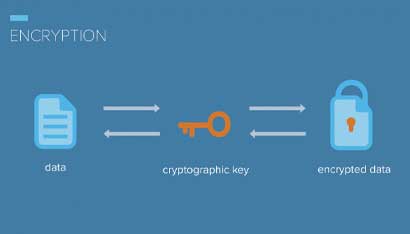

The blockchain is an encrypted database of transactions, which is stored in a database called a blockchain. In order to make a transaction in a cryptocurrency, you must be able to enter a code.

The code is the system that determines whether a transaction is legitimate or not. It also helps the network avoid double-spending and other scams. This feature allows you to send and receive cash without any third-party interference.

Conclusion

A blockchain is a database that stores the blockchain of all the transactions that take place on it. It is similar to a decentralized bank ledger. All users can access the ledger, and all of them are able to see what other users are doing.

A blockchain is a decentralized database, so it can be viewed by anyone, including other users. This means that a transaction is impossible to trace. A transaction is anonymous if the sender is unaware of it.